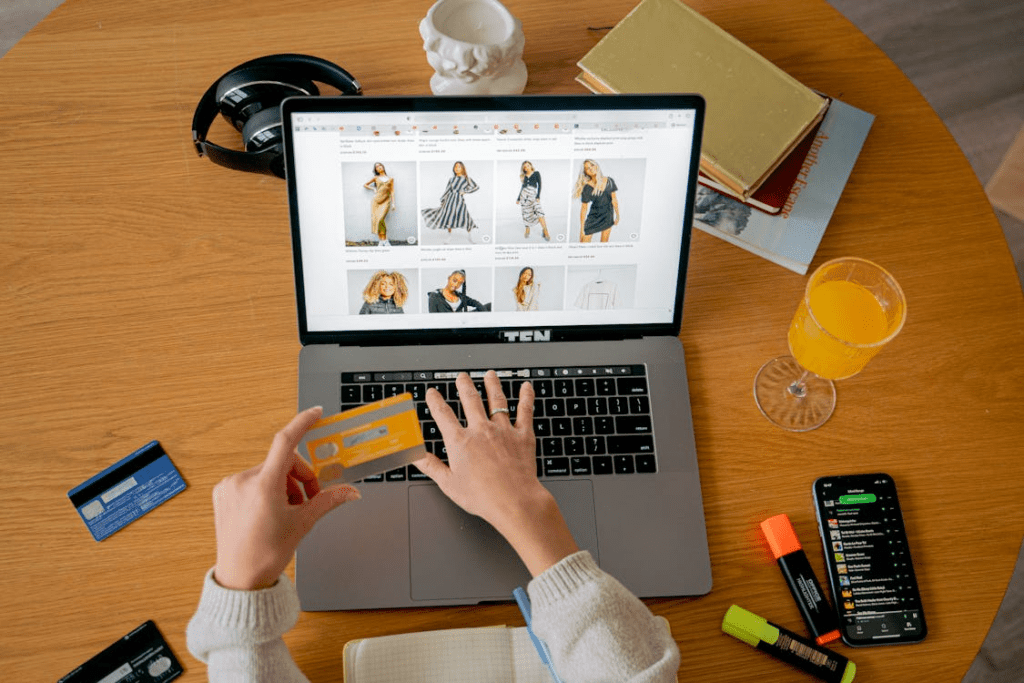

Is a debit card safe for online shopping? This is one of the biggest concerns when it comes to online transactions, and it’s no surprise. With payment fraud on the rise and card fraud being one of the leading types of fraud, you want to know if you can enter your card details on websites to pay for goods and services without risk. Generally, debit cards are safe to use online, but they come with potential dangers and vulnerabilities.

In this article, we address your concerns by answering the question: “Is it safe to use a debit card online?” We also:

- Share tips on how to use your debit card online safely

- Discuss steps to take if your debit card is stolen

- Offer a solution for safer storage of funds

Are Debit Cards Safe To Use Online? 3 Factors To Consider

Making payments with an online debit card is generally safe, but you should know what it involves to understand why it could also be risky.

When you want to make online debit card payments, you must share your card details and other financial data with the payment service. Doing this puts sensitive information at risk of falling into the wrong hands if you are exposed to a data breach.

If cybercriminals gain access to your financial data, you could fall victim to identity theft or debit card fraud. Since debit cards are directly linked to your bank, you also face the danger of your account being drained even before you realize what’s happening.

If you’re trying to decide whether you should use your debit card for online payment, consider these three factors:

- Potential of losing your funds

- Liability charges

- Long road to dispute the claim

Potential of Losing Your Funds

If you use a credit card for online purchases and fall victim to fraudsters, it’s highly unlikely that they will be able to access funds from your bank account. Your checking account remains unaffected since it’s not connected to your credit card. With a debit card, it’s different.

If a bad actor gets access to your debit card and your sensitive information, they could empty your account, leaving you with overdraft charges or failed payments, especially if you have recurring payments set up.

Liability Charges

Some banks may hold you liable if a fraudulent debit card transaction occurs on your card. The Electronic Fund Transfer Act (EFTA) categorizes liability claims into different levels depending on how long it takes you to report the crime.

See the charges you may face in the table below:

| How Long It Took To Report | Liability Charge |

| Before fraudulent transactions | No charge |

| Within 2 days | $50 |

| Within 60 days | $500 |

| After 60 days | Unlimited |

Fraud protection on debit cards is less stringent than credit cards. Still, you face more liability charges when fraud occurs on your debit card. If you fail to notice or forget to report that your debit card is compromised or stolen, federal law and most bank policies are not designed to protect you.

Long Road To Dispute the Claim

The process of proving that you’re innocent of debit card fraud is a bit winded and complicated, unlike credit card fraud claims. Here’s what it entails:

- You begin by filing a report with your card provider and wait for them to initiate an investigation

- The debit card provider will not issue you a credit to cover your lost funds, unlike credit card providers

- You have to wait until the debit card company confirms you were a victim before you get a chance to receive your refund

Debit card disputes are handled individually, and the investigation process is not geared toward favoring you, the consumer.

The Safe Way To Use Debit Card Online—4 Tips

Knowing the risks and potential aftermath of using debit cards online, it’s important to play it safe if you have to use them. Here are four rules to follow to protect your online debit transactions:

- Frequently review your bank statements

- Never use public Wi-Fi to transact

- Avoid unsecured e-commerce sites

- Use virtual cards where possible

Frequently Review Your Bank Statements

The earlier you discover fraudulent activity on your account, the faster you can mitigate the damage it could cause. Make it a habit to frequently review your bank statements—at least once or twice a week. This will help you spot unauthorized transactions or suspicious activity that could be fraud signals. Promptly reporting it also reduces your liability charges.

Never Use a Public Wi-Fi To Transact

Public Wi-Fi is more vulnerable to hackers and can be easily intercepted while you make financial transactions. Whenever you’re checking your account balance, paying bills, or shopping with your debit card, use a password-protected network. This reduces the chance of hackers stealing your information.

Avoid Unsecured E-Commerce Sites

One of the ways to identify an unsecured site is the lack of the letter “s” following “http” in the URL. The “s” indicates that the site is protected with a higher level of security and is safer to browse on. The padlock sign is another symbol of protection on e-commerce sites. If you must use your card to shop online, ensure these symbols are included.

Use Virtual Cards Where Possible

Virtual cards have unique card numbers generated for specific online transactions. They’re essentially one-time cards that become obsolete after the transaction. A virtual card keeps your primary card details safe when you shop online since they’re not connected in any way.

This means that if you enter a virtual debit card number, and the website becomes compromised by fraudsters, your debit card information will not be at risk.

Steps To Take if Your Debit Card Is Stolen or Compromised

If you discover that your debit card has been stolen or notice unauthorized debits on your account, it’s time to take these next steps:

- Report to the financial institution—Contact your bank or debit card provider immediately after you become aware of the incident. Delaying doing this could lead to potential identity theft, loss of funds, and unwanted charges

- Report to the police—File a police report if your card gets stolen. Make sure to keep a copy of the report, too, as this could help your reimbursement requests during the fraud investigation

- Update your password—If you still have access to your debit card account, change the password to a more secure and unique one to make it difficult for hackers to penetrate. Consider using a password manager to create and save strong passwords that keep fraudsters out

- Use more secure storage for your funds—A compromised debit card puts you at risk of losing all your savings in seconds. Get one step ahead of the scammer by moving your funds out of your savings account into a fraud-protected storage location like FortKnox